Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Posted Saturday, January 4, 2025

Table Of Contents

Here are some key takeaways-

Here are some key takeaways-

100% Business Expenses: These should be paid directly by the business (e.g., business meals, advertising).

100% Personal Expenses: These should be paid by the individual and not reimbursed by the business (e.g., gym memberships, personal subscriptions).

Mixed Use Expenses: These should be paid personally and then reimbursed by the business based on the business-use percentage (e.g., cell phone, internet).

Home Office: Reimbursement based on the percentage of the home used for business purposes (e.g., mortgage interest, utilities).

Cell Phones and Internet: Business-use percentages should be reasonable, with documentation to support the chosen split between personal and business use.

Mileage: If a personal car is used for business, the business can reimburse for mileage or a percentage of the car’s operating costs.

What’s the big deal? The big deal is that the IRS considers any reimbursement to be taxable income unless a proper Accountable Reimbursement Plan is adopted and implemented.

Also, the days of deducting these employee business expenses on Form 2106 are gone after the Tax Cuts and Jobs Act of 2017. As such, an Accountable Plan is needed now more than ever.

We designed a fancy MS Excel spreadsheet where you can enter your mixed use expenses. We suggest detailing your expenses and reimburse yourself through your Accountable Plan once every quarter- it is good accounting to stay on top of this, and memories tend to fade. More importantly, it helps with tax planning.

We designed a fancy MS Excel spreadsheet where you can enter your mixed use expenses. We suggest detailing your expenses and reimburse yourself through your Accountable Plan once every quarter- it is good accounting to stay on top of this, and memories tend to fade. More importantly, it helps with tax planning.

It is unfortunately too common when a business owner tells us he or she is making $100,000 after expenses throughout the year, and then during tax preparation he or she tells us about a $20,000 Accountable Plan reimbursement. It creates a big refund, sure, but it is not good tax planning.

Like any spreadsheet, it is only meaningful to the spreadsheet designer. So, we’ve created directions on using our Accountable Plan Worksheet and Reimbursement template. If you hate it, please kindly let us know. If you like it, simply send donuts and we’ll receive the message. Pictures of donuts don’t count.

There are potential problems with multiple owners when balancing Accountable Plan reimbursements. Let’s say your home office is 250 square feet and your home is 2,500 square feet. That is 10% business use. But your partner lives in an apartment, and her business use percentage is 25%. But! You have a mortgage and property taxes, whereas your partner pays rent. How do we keep that equitable? Tough!

There are potential problems with multiple owners when balancing Accountable Plan reimbursements. Let’s say your home office is 250 square feet and your home is 2,500 square feet. That is 10% business use. But your partner lives in an apartment, and her business use percentage is 25%. But! You have a mortgage and property taxes, whereas your partner pays rent. How do we keep that equitable? Tough!

Similar to automobiles, we can establish a not-to-exceed reimbursement limit but doesn’t that hose the owner who has more expenses? It certainly does.

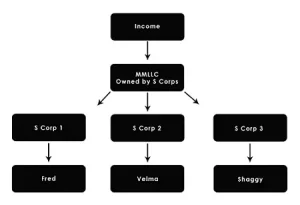

There is another solution where each owner operates an S corporation that provides management or other services to the primary entity. We refer to this as the Mothership Baby S Corp construct.

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Taxes are complicated. We make them simple. Get in touch with a pro here at WCG!

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Notifications